Fall Capital Markets Update

Productivity and Delta Variant

Historically in commercial real estate as well as in capital markets, summer has seen significant productivity slump. However, in 2020 and 2021 spring and summer were particularly slow from a productivity standpoint with pandemic related virtual learning and work from home crowd. Many companies are starting to call back employees in the offices although Delta Variant is putting a slight damper on the ‘going back to office’ phenomenon. Work of home or office, there will be less distractions for market participants to work. Soaring productivity along with ample liquidity in the markets will create deal activity in the commercial markets like we have never seen before.

Transitory Inflation, Permanent Inflation, Asset Inflation, Consumer Price Inflation and Rates

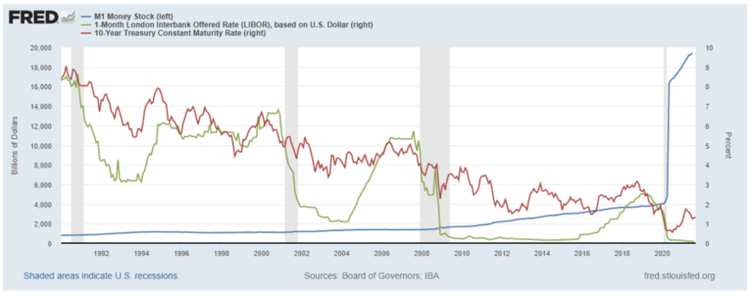

Our view at Mag Mile Capital is that some inflation will be permanent because of increased money supply in the system (see below graph on M1 since they began tracking). Compared to the money supply, below graph shows both short term and long term interest rates. This mismatch could be a perfect set up for Asset Price inflation. Consumer Price inflation will be transitory and prices for most of the consumer goods will either settle back to original (pre-pandemic) levels or slightly higher than original levels. However, due to increased liquidity and all-time low interest rates, there will be a sustained demand for stable yielding commercial real estates. Asset prices will favor particularly those types of real estate that has ability to increase rents. Lenders and Equity providers are already taking this view into account. Clients are rushing to refinance their assets to permanent financing for lower rates. In an inflationary scenario, Optimal Capital Structure Theory suggests that prudent debt on income producing assets is the best way to maximize future returns.

Refi vs. Sale

In a backdrop explained above along with lower level of inventory, our clients are rushing to refinance, take out as much imputed equity as possible in a form of tax free cash out, and lock in low interest rates for as long as possible (in most cases 10 years fixed rate). Investment Sales brokers and advisors are finding themselves competing against mortgage lenders because refinancing is becoming a top choice for real estate owners.

Hot Food Groups of CRE

Multifamily assets continue to be the darling of capital markets. Agency programs along with attractive CMBS, non-CMBS and Insurance Company lenders are piling on cash to lend on multifamily and industrial assets. Other trendy asset classes from a capital markets vantage point are built to rent (B2R) single family or horizontal housing communities for rent, self-storage assets, and mobile home and RV parks. Hospitality is back, most lenders have restarted to close hotel transactions. Rating agencies and lenders have adapted to gloss over 2020 performance for hospitality assets and look at 2019 performance as a baseline. Retail is also doing better than it was doing last year in middle of the pandemic. Office sector still lags with some covid clouds hovering over it. Overall most sub groups of CRE have recovered and capital markets lenders looking to fill up their balance sheets with healthy loans again.

CMBS, LifeCos, Debt Funds, and Balance Sheet Lender Trends

CMBS continues to be one of the most active asset classes as investors line up to generate stable yield. CMBS lenders are active again with spreads being all-time low due to high demand for collateral. CMBS lenders are not stretching the risk spectrum and highly relying on the appraisals to make their credit decisions. CMBS is lending 65% to 75% on most assets with in-place cash flow. Life Insurance Companies are also once again actively lending in for healthy real estate deals at leverage levels between 55% to 75% of value depending on the asset sub class. Debt Funds are also actively lending on deals that have realistic business plans. Properties with in-place cash flows are typically seeing interest rates in 3% to 5% range from debt funds. However, there are many debt funds in the market lending at 6% to 9% interest rates on properties that need more heavy lift and have storied business plans. Many Balance Sheets lenders that aim to be CMBS competitors have also emerged in recent history offering low fixed interest rates on non-recourse basis. Regional, community banks and credit unions are also offering recourse loans at competitive interest rates.

Equity Investors as well as Mezzanine lenders are also actively back in the game. Capital Markets are back to functioning at a healthy pace with cautiously optimistic outlooks at most shops.